Quote for the day

“I am a firm believer in luck and the harder I work the more I have of it.”

- Thomas Jefferson

“I am a firm believer in luck and the harder I work the more I have of it.”

- Thomas Jefferson

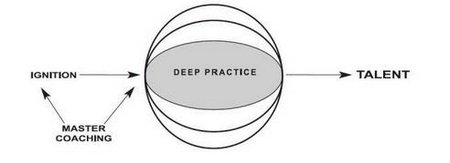

This book makes a case that talent is something else besides the nature and nurture stuff. Author based on his field research says that there are three ingredient’s to talent which are

Deep Practice

Ignition

Master Coaching

Deep practice involves struggling in a targeted way so that the learning happens at an accelerated pace. It is not usual “practice, practice , practice” mantra BUT one needs to stretch to reach a specific target and keep learning in the process. Roger Federer,for example does not play 1000’s of shots each day. He practices for a few hours and works on his timing. So, deep practice at the outset is a little different where one can describe it as error induced learning. It involves three stages as described in the book. Chunking the task + Repeating it + Learning to feel it.

“Good or bad, moral or immoral, people are going to make markets and trade via computers, and this is a natural area of financial engineers,”

-Emanuel Derman

The only reason I chose to read this book on a weekend was to verify the null hypothesis of the author, " an intuitive guide" :) Well, intuition and econometrics are kind of animals that don’t sleep together that well in the SAME book. Either econometrics books are very math/probability oriented OR they are “stats for dummies” types. I had tons of other things to do on this weekend, but took a peek in to this ~100 page double line spacing book,just out of curiosity.

Simulator should be ONE of the tools , a trader uses regularly, especially a newbie.Why ?

Here is a nice argument FOR it - The Talent Code Revisted

“In three words I can sum up everything I’ve learned about life: it goes on.”

– Robert Frost

The only reason I chose to read this book on a weekend was to verify the null hypothesis of the author, " an intuitive guide" :) Well, intuition and econometrics are kind of animals that don’t sleep together that well in the SAME book. Either econometrics books are very math/probability oriented OR they are “stats for dummies” types. I had tons of other things to do on this weekend, but took a peek in to this ~100 page double line spacing book,just out of curiosity.

Here is a nice paper that I have stumbled on, “The Scientific Illusion in Empirical Macroeconomics ” by Lawrence Summers.

Basic argument of the paper is :

Formal econometric work where elaborate technique is used to either apply theory to data or to isolate the direction of causal relationships where they are not obvious a priori virtually always fails. If this argument is accepted it suggest that in evaluating empirical work we should begin by asking different questions than the ones usually posed.Instead of considering the methods employed, we should ask whether the fact reported is an interesting one that affects our view of how the economy operates. Does it affect our belief about a substantive question?

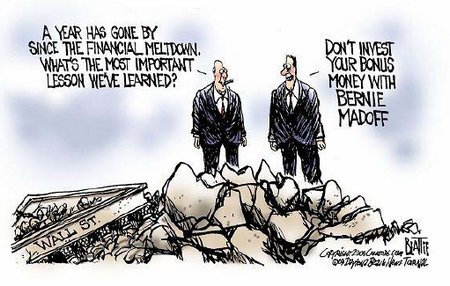

A nice illustration about the current US situation

What lies behind you and what lies in front of you, pales in comparison to what lies inside of you.

- Ralph Emerson.

Mathematics is discovered in much the same way as any other science - by experimentation (here, simulation) followed by confirmation (proof). All too often, students think mathematics was created by divine inspiration since, by the time they see it in class, all the “dirty work” has been “cleaned up.”

- Prof Alan Levine

I guess the “dirty work” is where all the fun lies !

Last week has been a pretty unproductive week. Fell ill on Tue and Wed. Barely managed to work for a few hours on Thu. But by Friday I was back to normalcy. Generally one of the ways I get over from an inertia state to an active state is to read something interesting. So, picked up this frequel( from the back cover : nice name for freakonomics sequel ). I knew there was a lot of controversy relating to this book. Some people argued that authors got it completely wrong as far as global warming is concerned. Some argued it was a hotch potch of some articles.

Last week has been a pretty unproductive week. Fell ill on Tue and Wed. Barely managed to work for a few hours on Thu. But by Friday I was back to normalcy. Generally one of the ways I get over from an inertia state to an active state is to read something interesting. So, picked up this frequel( from the back cover : nice name for freakonomics sequel ). I knew there was a lot of controversy relating to this book. Some people argued that authors got it completely wrong as far as global warming is concerned. Some argued it was a hotch potch of some articles.

You can’t treat cancer with pain killers. That’s what is happening to US Banking.

- Taleb

Michael Lewis, needs no introduction . His previous works have been best-sellers. When he writes a book about subprime crisis, I was expecting a dot-com esque narration of subprime mess with all the ingredients of a thriller movie ride.It turned out to be exactly what I expected.This book is essentially a collection of articles, essays by various people before panics, be it the 1987 crash | asian currency crisis | dot-com bust | the recent sub-prime bust. Reading this book is like bringing old newspaper articles, magazines from your attic to go over what people said about various crisis situations.

Via Berkshire Hathaway 2008 Report :

The Black-Scholes formula has approached the status of holy writ in finance, and we use it when valuing our equity put options for financial statement purposes. Key inputs to the calculation include a contract’s maturity and strike price, as well as the analyst’s expectations for volatility, interest rates and dividends.If the formula is applied to extended time periods, however, it can produce absurd results. In fairness,Black and Scholes almost certainly understood this point well. But their devoted followers may be ignoring whatever caveats the two men attached when they first unveiled the formula.

Any poet, even the most allergic to mathematics, has to count up to twelve in order to compose an alexandrine.

- Raymond Queneau

For the last one month I was completely occupied with work . Weekdays and Weekends flew away before I realized that it has been quite sometime since I had read any book. This weekend , being a long weekend , decided to spend my time reading a book on ambiguity. I stumbled on to a reference to this book on some blog and was intending to read at some point in time. A nice holiday break and festive mood around was good enough to motivate me to read this book, which was touted as a mathematical novel.

I have often wanted to underline statements / words in a pdf but the security settings of most of the online documents prevented me from doing so. I like the content being in a word doc .

Found a nice software (free) which converts a pdf in to word doc. I am pretty happy with the quality of the output.

Link : HelloPdf

One of my research colleagues ( a Phd in Math) wanted to get in to industry. However her desire came at a rather disturbing economic time( 2008 ) . She interviewed at various fund houses but the job situation looked grim. However she managed to get 2 offers. One from her home land , a plum treasury related role and other a job at Galleon hedge fund, NYC. She joined Galleon.The job responsibility at Galleon was exciting as it was high frequency options trading strategies and she was kicked about it. I felt good about the whole stuff as she got in to a role which she wanted to do . The fact she lived in my neighborhood at NJ made me generally enquire about her work etc as she had moved from a hard core research oriented role to a role which involved taking daily trading calls. She seemed happy doing intra-day trading.

Take any asset , Every investor has a specific idea of return as it is based on the expected holding period, ability to short sell, turn over of the asset etc. If one were talk about returns, it is very difficult to give a generic metric. There are umpteen ways to calculate returns as one can imagine. For example,

In Indian markets, there is no doubt that NIFTY, NIFTY Jnr index assets figure amongst the sought after assets. Also with Gold witnessing a dramatic rise year after year , it is attracting hordes of investors too. Lets look at these assets from a risk return perspective and understand the importance of the scale for returns calculation

Noah’s Ark was built by amateurs. It took professionals to build the Titanic.

Your net worth to the world is usually determined by what remains after your bad habits are subtracted from your good ones.

_- Benjamin Franklin

_

One of my friend’s brother works for the stock exchange and I happened to chat up with him about technical analysis. I have been told that a user interface would be available soon on the web site of the stock exchange. He asked me my thoughts on the some of the TA graphs and the type of charts I would be interested in looking at. This post is a summary of my thoughts on the same.

Why “portfolio optimization” as a discipline , needs to develop a LOT ?

Link : 1/N , an LBS paper reports that equally weighted portfolio is good enough!

NYT article says :

_The F.T.C. said that beginning on Dec. 1, bloggers who review products must disclose any connection with advertisers, including, in most cases, the receipt of free products and whether or not they were paid in any way by advertisers, as occurs frequently. The new rules also take aim at celebrities, who will now need to disclose any ties to companies, should they promote products on a talk show or on Twitter. A second major change, which was not aimed specifically at bloggers or social media, was to eliminate the ability of advertisers to gush about results that differ from what is typical — for instance, from a weight loss supplement.

_

I am definitely against this!. Shouldn’t crap reviews/content written , be killed by the “wisdom of crowds” funda. Why is there a need for a regulation ?

“A good traveler has no fixed plans, and is not intent on arriving.”

_

- Lao Tzu_

My random thoughts/questions about portfolio optimization , some of which got answered based on the work I had been doing in the last 2-3 weeks. Some remain unanswered!.

Charles Stein stunned the statistician community when he first published a paper which showed that average of past events is not the best predictor of future event.

Here is the original article which uses baseball stats to give an insight in to the paradox – Paradox in Statistics

This is a new addition to my diagnostic tool kit. I had never used Box Percentile plot before. However this week, I had to look at outliers in a data. Histograms are not that good for outliers. Box Plots, same story(though whiskers in the box plot are useful in getting an idea about the data points 1.5 IQR away from the boxes). I usually prefer Box plots for the simple reason that it gives a sense of the data from a quartiles perspective. . However most of the times you are interested in knowing more about them from a diagnostic perspective.

Via Mihaly Csikszentmihalyi((pronounced “CHICK-sent-me-high-ee”) , Chicago professor and the author of one the most influential books,"FLOW " says , being in flow means :

A programmer can write tens of thousands of lines of code, and produce a lot of software that works. A less productive coder can write a tenth of the lines, perhaps even editing down what she writes so that there’s less code, but they’re better written. This small program might be the most useful thing on many people’s computers, flawless code that just works.

- Leo Babauta

This is what an 8 year slog with Abacus/ Soroban (as called in Japan) can enable one to do .

Look at the video and watch how one can visualize huge mental arithmetic problem..It was a jaw dropping experience to watch kids do this!!

While using R, there are umpteen instances one has to browse for the relevant package for a dataset / function / class. It is a time consuming activity….But now, thanks to the authors of sos library its an effortless exercise!…

Let’s say you want to use robust estimator for a sample and you want to know whether R community has it already or not. With just three lines of code, you get a ton of summary relating to what you want to search

All models are wrong, some models are useful.

- George E. P. Box

Everyone who goes through the BSchool /CFA rut knows about mean variance optimization . Some of them might know that it does not work in the practical world. So, what if noble prizes have been awarded!! It doesn’t work in practice…Like all models, however, it does give a framework to think about and nothing more than that….So, What’s the alternative ? If you are given a couple of assets and are asked to create an asset mgmt plan, how would you go about it ? Pick up any random Bschool student and ask this question and I am certain that only a few of them would be able to answer coherently..Why ? Finance education is stuck in gaussian world!! anyways, the point of this post is to summarize this book which suggests alternatives. I came across a reference to this book in a paper and was curious to know more about it, almost a year ago. Was intending to use Bayesian estimates if ever I had to solve a portfolio allocation framework. This weekend , I had decided to take a look at this book out for sheer curiosity. What I was found in this book was a fascinating critique of classic MV solution and more than that, a statistically solid approach to the MV optimization problem.

Never bothered to think about this aspect until today, when the choice of the format made a ton of the difference to the output!

Via C# Corner :

First off, why use PNG instead of GIF? Probably the most important reason is that GIF supports a maximum of 256 colors. The second reason is Unisys has a lockdown on the rights to LZW compression which the GIF format can, and usually does use. PNG overcomes the color depth hurdle by providing up to 48Bpp (bits per pixel). Just as importantly, the PNG format is patent-free and available for use by anyone.

Numbers do not lie, but they have the propensity to tell the truth with intent to deceive

-- E. T. Bell

It has been 2 months since I have coded a single line of C# . Today I have to use it again for some reason and I seem to have forgotten everything about it. My short term memory is killing me !.. Every once in a while I face this problem. A month ago, I forgot ruby syntax. It took me almost a day to get back to speed. A few months ago, same thing happened with PostgreSQL syntax. 3 months back with VBA Syntax!!

It has been more than one and half months since I have read any book. Was involving in developing some stuff @work, so was completely immersed in it. Decided to read this book on a beautiful Saturday.

Came across this book in an NY times article and was looking forward to read the book, as it was relating to an aspect which is close to my heart, hacking.Hacking in geek’s jargon is ripping apart software, packages, libraries, things and understanding stuff at level 0. In some sense,I guess there are two types of people, first kind who do not want to get their hands dirty a lot and would rather assemble, manage a set of people to accomplish some task, second kind are those who want to hack things and build things from scratch. By the kind of education I have undergone, I should be doing the former but I have found joy in the latter activity. In that sense, I could relate to the author was a Chicago Phd , academic, whom one would expect to write papers, do research and be a professor. Instead he chooses to become a mechanic. Why ? This book answers that question and much more. Author has organized the book in such a way that it traces author’s experiences from being a young apprentice in a repair shop , to being a PhD from Chicago, to working in a cubicle, to finally coming round the circle to repair shop again.

Via Jayanth:

A real hero never says anything without thinking and never thinks after saying

We are drowning in information and starving for knowledge.

–Rutherford D. Roger