Brownian Motion Converges to Std Normal

Purpose

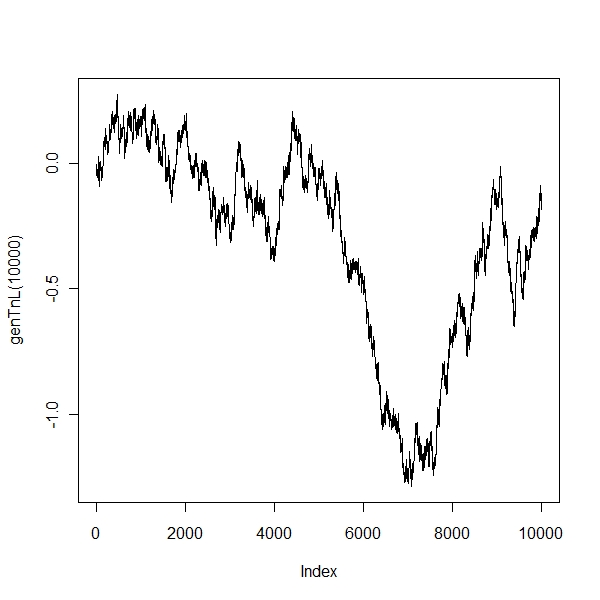

If you take a symmetrical random walk and scale it, it becomes a browninan motion.

> par(mfrow = c(1, 1))

> library(ConvergenceConcepts)

> genTnL <- function(n) {

+ delta <- 1/n

+ ds <- sqrt(delta) * rnorm(n)

+ S <- cumsum(ds)

+ Z <- S/(sqrt(delta) * sqrt(n))

+ return(Z)

+ }

> plot(genTnL(10000), type = "l") |

The above clearly shows that as you increase sample paths, the scaled brownian motion converges to a standard normal.