Spurious Regression - Visualization

Purpose

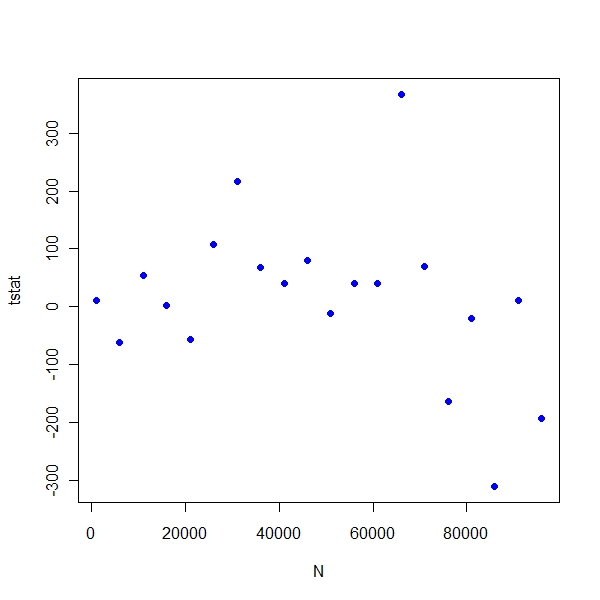

If two non stationary series are regressed, the t stat increases

> set.seed(1977)

> N <- seq(1000, 1e+05, 5000)

> results <- numeric(0)

> for (i in seq_along(N)) {

+ y <- cumsum(rnorm(N[i]))

+ x <- cumsum(rnorm(N[i]))

+ fit.sum <- summary(lm(y ~ x))

+ results <- c(results, coef(fit.sum)[2, 3])

+ }

> plot(N, results, pch = 19, col = "blue", ylab = "tstat", xlab = "N") |

clearly t stat diverges

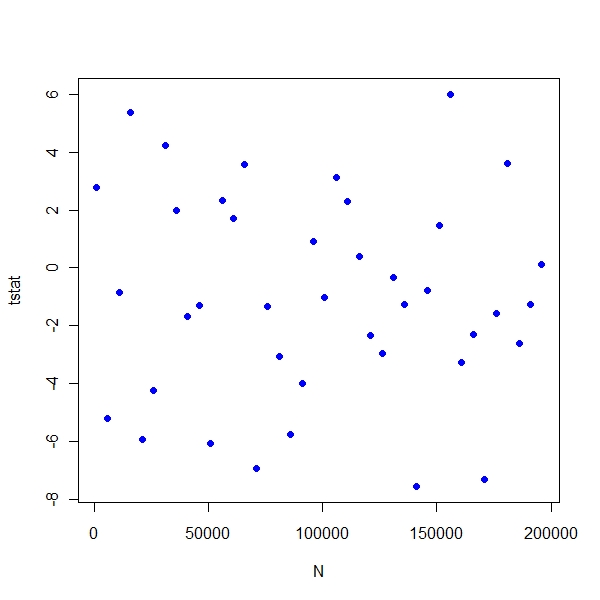

If two stationary series are regressed, the t stat increases

> set.seed(1977)

> N <- seq(1000, 2 * 1e+05, 5000)

> results <- numeric(0)

> for (i in seq_along(N)) {

+ y <- arima.sim(n = N[i], model = list(ar = 0.9))

+ x <- arima.sim(n = N[i], model = list(ar = 0.95))

+ fit.sum <- summary(lm(y ~ x))

+ results <- c(results, coef(fit.sum)[2, 3])

+ }

> plot(N, results, pch = 19, col = "blue", ylab = "tstat", xlab = "N") |

clearly t stat converges when you regress 2 stationary processes.