Heteroskedasticity Tests

Purpose

To compare various Heteroskedastic tests

Simulate data

> set.seed(1977)

> n <- 1500

> beta.actual <- matrix(c(2, 3), ncol = 1)

> beta.sample <- cbind(rnorm(n, beta.actual[1]), rnorm(n, beta.actual[2]))

> error <- c(rnorm(n/2), rnorm(n/2, 0, 3))

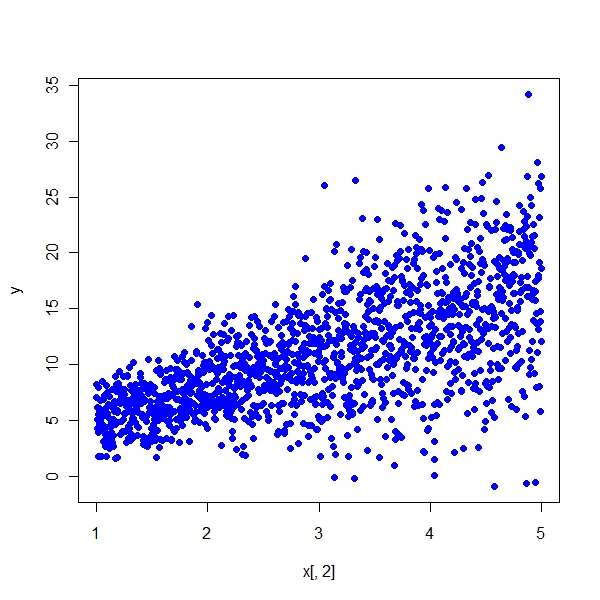

> x <- cbind(rep(1, n), seq(from = 1, to = 5, length.out = n))

> y <- x[, 1] * beta.sample[, 1] + x[, 2] * beta.sample[, 2] +

+ error

> plot(x[, 2], y, pch = 19, col = "blue")

> summary(lm(y ~ x + 0))

Call:

lm(formula = y ~ x + 0)

Residuals:

Min 1Q Median 3Q Max

-17.01448 -2.13231 0.07604 2.19407 17.87364

Coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2.08587 0.28936 7.209 8.93e-13 ***

x2 2.91157 0.09001 32.348 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 4.028 on 1498 degrees of freedom

Multiple R-squared: 0.888, Adjusted R-squared: 0.8878

F-statistic: 5936 on 2 and 1498 DF, p-value: < 2.2e-16

> coef(lm(y ~ x + 0))

x1 x2

2.085867 2.911567 |

Goldfeld Quandt Test

> gqtest(y ~ x[, 2])

Goldfeld-Quandt test

data: y ~ x[, 2]

GQ = 4.3728, df1 = 748, df2 = 748, p-value < 2.2e-16 |

Breusch-Pagan Test

> x.t <- rep(c(-1, 1), 50)

> err1 <- rnorm(100, sd = rep(c(1, 2), 50))

> err2 <- rnorm(100)

> y1 <- 1 + x.t + err1

> y2 <- 1 + x.t + err2

> bptest(y1 ~ x.t)

studentized Breusch-Pagan test

data: y1 ~ x.t

BP = 12.1028, df = 1, p-value = 0.0005035

> bptest(y2 ~ x.t)

studentized Breusch-Pagan test

data: y2 ~ x.t

BP = 1.2061, df = 1, p-value = 0.2721 |

White test

> library(lmtest)

> bptest(y ~ x[, 2] + I(x[, 2]^2) + 0)

studentized Breusch-Pagan test

data: y ~ x[, 2] + I(x[, 2]^2) + 0

BP = 176.1623, df = 1, p-value < 2.2e-16 |

Null says same variance and the above p value says that we can reject null

> library(fArma)

> n <- 1500

> beta.actual <- matrix(c(2, 3), ncol = 1)

> beta.sample <- cbind(rnorm(n, beta.actual[1]), rnorm(n, beta.actual[2]))

> error <- c(rnorm(n/2), rnorm(n/2, 0, 3))

> x <- cbind(rep(1, n), seq(from = 1, to = 5, length.out = n))

> er.ar <- arima.sim(list(order = c(1, 0, 0), ar = c(0.9)), n = n)

> y <- x[, 1] * beta.sample[, 1] + x[, 2] * beta.sample[, 2] +

+ er.ar

> plot(x[, 2], y, pch = 19, col = "blue")

> summary(lm(y ~ x + 0))

Call:

lm(formula = y ~ x + 0)

Residuals:

Min 1Q Median 3Q Max

-14.82168 -2.49701 0.02933 2.46448 13.68807

Coefficients:

Estimate Std. Error t value Pr(>|t|)

x1 2.15368 0.28692 7.506 1.04e-13 ***

x2 3.04792 0.08925 34.151 < 2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 3.994 on 1498 degrees of freedom

Multiple R-squared: 0.8979, Adjusted R-squared: 0.8977

F-statistic: 6584 on 2 and 1498 DF, p-value: < 2.2e-16

> dwtest(y ~ x + 0)

Durbin-Watson test

data: y ~ x + 0

DW = 1.4457, p-value < 2.2e-16

alternative hypothesis: true autocorrelation is greater than 0 |

Cochrane Orcutt Iterative Least Squares

> cochrane.orcutt.lm <- function(mod) {

+ X <- model.matrix(mod)

+ y <- model.response(model.frame(mod))

+ e <- residuals(mod)

+ n <- length(e)

+ names <- colnames(X)

+ rho <- sum(e[1:(n - 1)] * e[2:n])/sum(e^2)

+ y <- y[2:n] - rho * y[1:(n - 1)]

+ X <- X[2:n, ] - rho * X[1:(n - 1), ]

+ mod <- lm(y ~ X - 1)

+ result <- list()

+ result$coefficients <- coef(mod)

+ names(result$coefficients) <- names

+ summary <- summary(mod, corr = F)

+ result$cov <- (summary$sigma^2) * summary$cov.unscaled

+ dimnames(result$cov) <- list(names, names)

+ result$sigma <- summary$sigma

+ result$rho <- rho

+ class(result) <- "cochrane.orcutt"

+ result

+ }

> cochrane.orcutt.lm(lm(y ~ x[, 2]))

$coefficients

(Intercept) x[, 2]

2.132841 3.053598

$cov

(Intercept) x[, 2]

(Intercept) 0.14579406 -0.04230266

x[, 2] -0.04230266 0.01408982

$sigma

[1] 3.837711

$rho

[1] 0.276815

attr(,"class")

[1] "cochrane.orcutt" |